Welcome to glum’s documentation!

glum is a fast, modern, Python-first GLM estimation library. Generalized linear modeling (GLM) is a core statistical tool that includes many common methods like least-squares regression, Poisson regression and logistic regression as special cases. In addition to fitting basic GLMs, glum supports a wide range of features. These include:

Built-in cross validation for optimal regularization, efficiently exploiting a “regularization path”

L1 and elastic net regularization, which produce sparse and easily interpretable solutions

L2 regularization, including variable matrix-valued (Tikhonov) penalties, which are useful in modeling correlated effects

Normal, Poisson, logistic, gamma, and Tweedie distributions, plus varied and customizable link functions

Dispersion and standard errors

Box and linear inequality constraints, sample weights, offsets.

A scikit-learn-like API to fit smoothly into existing workflows.

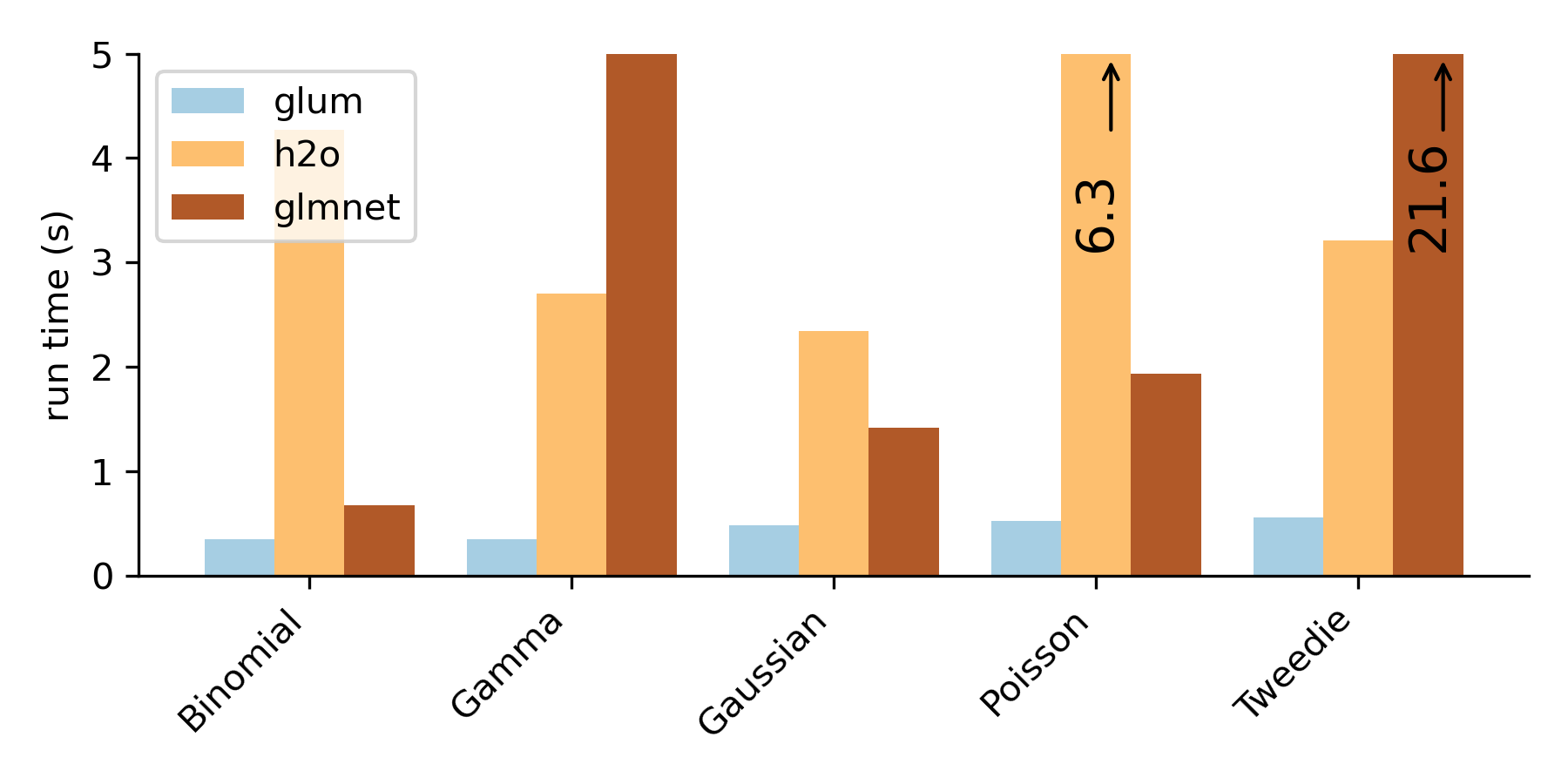

glum was also built with performance in mind. The following figure shows the runtime of a realistic example using an insurance dataset. For more details and other benchmarks, see the Benchmarks section.

We suggest visiting the Installation and Getting Started sections first.